This brings us to the generational gap that often goes unspoken, and the mindset shift that can transform everything.

However, let me say something that might sting a little. I say this because I care, and because I’ve sat across from hundreds of hardworking people who have asked me the same question—with the same defeated look in their eyes:

“Marcia, I make good money, and on top of that, I work hard. Given all this, why does owning a home still feel completely out of reach?”

The truth is, it’s not only the market. It’s not only inflation. And it’s certainly not just your salary. It’s something deeper, something that started long before you ever opened a bank account. You were never taught how to think about money. And that gap, that silent, generational gap, is costing you the life you deserve.

The Generational Money Gap Nobody Talks About

Most of us grew up in homes where money was either a source of shame, stress, or silence. “We don’t talk about money” was practically a family value. Your parents did the best they could, and their parents did the best they could as well. But generation after generation, the blueprint for building wealth, the one that leads to homeownership, equity, and financial freedom , was simply never passed down.

The people who grew up with that blueprint learned it right at the dinner table. From parents who casually explained what a down payment was, who pointed out interest rates in the newspaper, who reviewed their kids’ credit reports before they left for college. That’s a generational advantage that’s almost impossible to see from the outside, and nearly impossible to overcome if no one ever tells you it exists.

This isn’t about blame. It’s about awareness. Because once you see the gap, you can start to bridge it. And that bridge begins with one thing: changing the way you think about money.

Why “Earn More, Spend Less” Advice Keeps Failing You

Every personal finance guru says it: cut your lattes, budget harder, earn more. And look — those things matter. But they’re the tactics, not the strategy. They’re the tools, not the blueprint. And if you’re swinging a hammer without knowing what you’re building, you’ll exhaust yourself and have nothing to show for it.

The deeper problem isn’t behavior, it’s belief. If you were raised to believe that wealth is for “other people,” that homeownership is a lucky accident rather than an engineered outcome, that debt is always bad and credit is dangerous, then no budget spreadsheet is going to save you. You’ll find a way to self-sabotage every time you get close.

I’ve watched people earning $80,000 a year feel more financially hopeless than people earning $45,000 — because the ones earning less had someone teach them how to leverage what they had. Knowledge, not income, is the great equalizer.

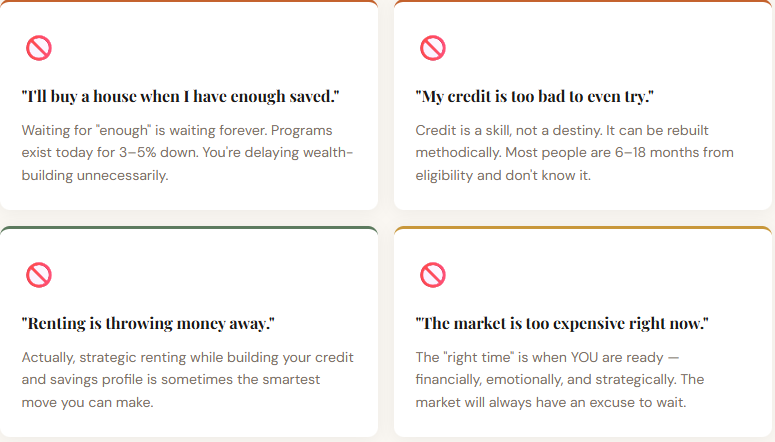

The 5 Money Beliefs That Are Blocking Your Front Door

These are the mindset blocks I see most often in the families I coach. Do any of these feel familiar?

What You Actually Need to Know (That School Never Taught)

Let’s get into the real education. The one that should have happened years ago. Here are the pillars of money thinking that lead directly to homeownership:

1. Credit is a Language — Learn to Speak It

Credit isn’t a judgment on your character. It’s a communication tool that tells lenders a story about your reliability. The question isn’t whether you have credit, but whether you’re fluent in it. Understanding utilization ratios, the weight of your payment history, and how to use credit cards strategically as tools instead of traps can change everything. With the right moves, a score of 580 today can become 680 in just twelve months.

2. Your Debt-to-Income Ratio Is More Important Than Your Credit Score

Most people obsess over their credit score and ignore their DTI. Lenders want to know: of every dollar you earn, how much is already spoken for? If 50% of your income goes to existing debt payments, you’ll struggle to qualify for a mortgage regardless of your score. This is about architecture — building a financial structure that can support a home loan.

3. Down Payment Assistance Is Real Money That Most People Leave on the Table

There are thousands of down payment assistance programs in every state across the country, including grants, forgivable loans, and matched savings programs. Many of my clients have received $10,000, $15,000, even $25,000 in assistance they didn’t even know existed. This money doesn’t come looking for you. You have to know it’s there and understand how to access it.

Ready to turn this knowledge into a plan? Marcia’s 90-Day Home Buying Challenge walks you through every step from credit to closing. Join Now →

4. Wealth is Built in the Gap Between What You Earn and What You Strategically Deploy

Building wealth isn’t about deprivation; it’s about intentionality. Every dollar should have a purpose: high-yield savings for your down payment fund, paying down revolving credit to lower your DTI, and knowing which debts to prioritize and in what order. This is financial choreography, and it’s something you can learn.

The Generational Cost of Waiting

Here’s what the math looks like when you delay homeownership by five years waiting until things “feel right”:

- Lost equity accumulation. A $250,000 home appreciates at an average of 4% annually. Over five years, that’s approximately $54,000 in wealth you didn’t build, wealth that would have been working for you, not for your landlord.

- Rising prices outpacing savings. If home prices increase faster than you can save, the goalpost keeps moving. You save $15,000 toward a down payment while prices rise by $30,000. You’re running backward.

- Rent increases eat your savings window. Rent goes up an average of 3–5% per year. The money you’re spending on rent increases could be building equity in a home you own.

- Broken generational cycle, or continued one. Every year you wait is another year your children grow up in a household without the tangible and psychological anchor of homeownership. The cycle either breaks with you or continues through you.

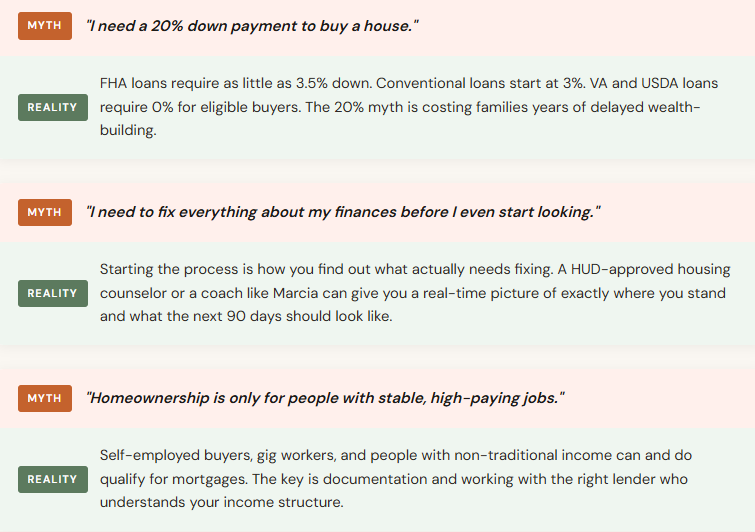

Busting the Myths That Are Keeping You Renting

What Closing the Gap Actually Looks Like

I want to tell you about someone I’ll call Destiny, a composite of dozens of women I’ve worked with over the years. She was 34, a single mom, renting a two-bedroom apartment for $1,400 a month.

Her credit score was 591, she had about $3,200 in savings, and she had convinced herself that homeownership was for “people like her friends, not people like her.”

Then she joined my program. We audited her credit, disputed three errors, and strategically deployed two secured cards.

Next, we identified a state-funded down payment assistance grant she qualified for and mapped out which debts to pay down first to bring her DTI into the qualifying range.

We got her pre-approved fourteen months later for a $210,000 home with $0 out of pocket at closing after assistance.

Destiny didn’t get lucky. She got educated. She got a plan. And she got to work.

That story isn’t rare. It’s repeatable. The only thing that changes is the name.

The Mindset Shift That Changes Everything

Here’s the reframe I want you to carry with you: homeownership isn’t a reward for financial perfection. It’s a tool for building the financial future you want. You don’t need to have it all figured out. What matters is having a direction, being willing to learn what you weren’t taught, and investing the next 90 days in understanding the path forward.

The generational gap is real. The systemic barriers are real. The disadvantages that come from growing up in a household where money was never discussed, those are real too. I’m not minimizing any of it. However, it is also important to recognize that this gap can be closed.

In one generation. In one decision. In one deliberate, strategic, supported step toward the front door of a home that belongs to you.

Your Next Step Starts Here

If you’ve read this far, it means something in you is ready. You don’t need more motivation; you need a map. That’s exactly what I’ve built in the 90-Day Home Buying Challenge. Over 90 days, I’ll guide you through the exact steps: the credit moves, the savings strategy, the lender conversations, and the assistance programs that turn “I can’t afford a home” into “I’m closing on a home.”

You were never taught how to think about money, and that ends now. Let’s start building something together.