By Marcia L Smith | Home Buying Coach and Financial Educator

Renting feels responsible. It feels flexible. For a lot of people, it even feels smart. No maintenance bills. No property taxes. No commitment. Just a fixed monthly payment and the freedom to pick up and move whenever life calls for it. On the surface, renting looks like the safe choice. And that is exactly why it is so dangerous.

Because here is what nobody tells you when you sign that lease. Every single month, you are making someone else wealthy. Every rent payment you hand over is gone forever. It builds no equity, creates no asset, and leaves nothing behind for your future. Meanwhile, the person cashing your check is building net worth, accumulating tax benefits, and watching their investment appreciate while you cover their mortgage.

I am Marcia L Smith, and I have coached hundreds of families through the home buying process. Furthermore, one of the most common things I hear from clients after they close on their first home is this: I wish I had done this sooner. Not because the process was easy. But because when they finally saw the real math, they realized how much they had been losing, quietly and consistently, every single month they stayed in their rental.

This post is about that math. All of it. The numbers nobody puts in front of you when you renew your lease. The cost of waiting that compounds silently year after year. And the clear, concrete picture of what homeownership can actually do for your financial future.

First, Let’s Talk About What Renting Actually Costs You

Most renters think about rent as a housing expense. A monthly cost of living, like groceries or a phone bill. That framing, however, is one of the most expensive mental mistakes you can make. Because unlike groceries, your rent payment is not just paying for something you need. It is actively funding someone else’s wealth-building strategy.

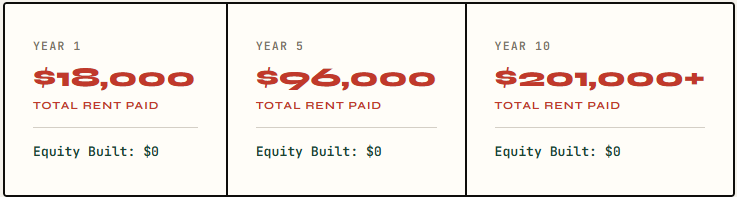

Consider this. The average American renter spends approximately $1,500 per month on rent. Over the course of one year, that is $18,000. Over five years, that is $90,000. Over ten years, that is $180,000. And over twenty years, assuming even a modest 3 percent annual rent increase, that number climbs well above $400,000.

Every single dollar of that is gone. There is no asset at the end. No equity. No return. Just receipts.

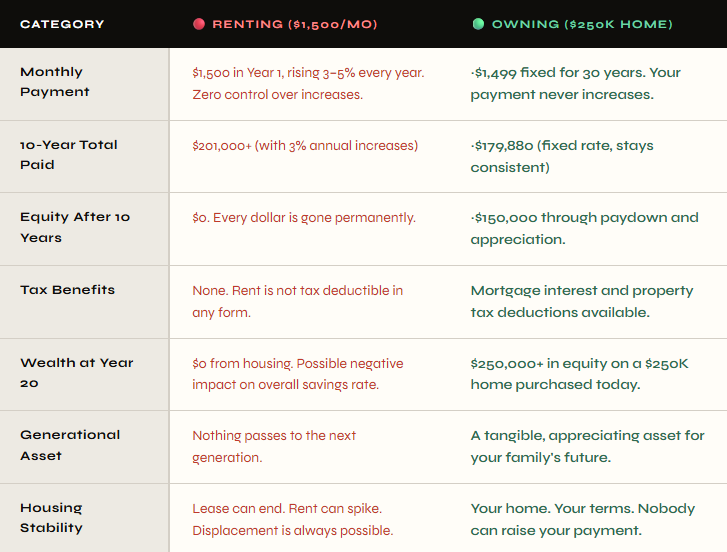

Now compare that to what a homeowner builds over the same period. On a $250,000 home with a 6 percent fixed mortgage rate, your monthly principal and interest payment is approximately $1,499. Nearly identical to that average rent payment. But the similarities stop there entirely. Because every month, a portion of that payment reduces your loan balance and builds equity. Meanwhile, the home itself appreciates in value. According to historical averages, home values in the United States increase by approximately 4 percent per year.

So at the end of year one, you are not just back to zero. You are ahead. You have built equity through loan paydown. You have gained value through appreciation. And you have access to tax deductions that renters simply do not have.

The 10-Year Wealth Gap: Renting vs. Owning

Let’s make this even more concrete. Here is what the numbers look like over a 10-year period, comparing a renter and a homeowner starting in similar financial positions.

The Renter spends $1,500 per month in year one. With a 3 percent annual rent increase, they are paying approximately $1,960 per month by year ten. Over the full decade, they spend a total of roughly $201,000 in rent payments. Their net housing wealth at the end of year ten is zero dollars.

The Homeowner pays approximately $1,499 per month in principal and interest on a $250,000 home throughout the decade. Their payment never increases because it is fixed. Over ten years, they have paid down approximately $30,000 of their loan balance. Additionally, at 4 percent annual appreciation, their $250,000 home is now worth approximately $370,000. That means their equity, the difference between what the home is worth and what they owe, is approximately $150,000.

To summarize: after ten years, the renter has spent over $200,000 and has nothing to show for it. The homeowner has spent a similar amount and has accumulated $150,000 in wealth.

That is a $150,000 difference. Built not through luck, not through a high income, and not through a windfall. Built simply by owning instead of renting.

To summarize: after ten years, the renter has spent over $200,000 and has nothing to show for it financially. The homeowner has spent a similar amount and has accumulated roughly $150,000 in wealth. That is a $150,000 difference built not through luck, not through a high income, and not through a windfall, but simply by owning instead of renting.

The Hidden Tax: How Annual Rent Increases Quietly Drain Your Future

One of the cruelest aspects of the renting cycle is how gradually and routinely rent increases happen. Each year, the landlord sends a notice. Your rent goes up by $50, $75, maybe $100. It feels small. It barely registers. And that is exactly what makes it so financially devastating over time.

Here is what that modest 3 percent annual rent increase actually looks like when you follow the numbers forward.

By year twenty, the renter is paying $2,634 per month for the same apartment they moved into paying $1,500. Meanwhile, the homeowner is still paying $1,499, which is the same payment they made on day one. Furthermore, the homeowner’s home has now doubled in value, and they have built over $250,000 in equity.

The homeowner did not get richer because they earned more. They got richer because they stopped letting their housing payment work for someone else’s future and started letting it work for their own.

What Home Equity Actually Looks Like Year by Year

Equity is the word that changes everything for first-time buyers when they finally understand it. Equity is simply the difference between what your home is worth and what you still owe on it. It is real, accessible wealth that grows in two ways simultaneously: as you pay down your mortgage and as your home appreciates in value.

Here is what equity accumulation looks like on a $250,000 home purchased today at 6 percent interest, assuming 4 percent annual appreciation.

Consequently, equity is not just a number on a statement. It is usable wealth. Homeowners can borrow against their equity for renovations, education, or emergencies. They can sell and walk away with a substantial down payment on their next, larger home. They can pass it to their children as a financial foundation that no lease renewal can ever create.

Ready to start building equity instead of paying rent?

Marcia’s 90-Day Home Buying Challenge gives you the exact plan to get there.

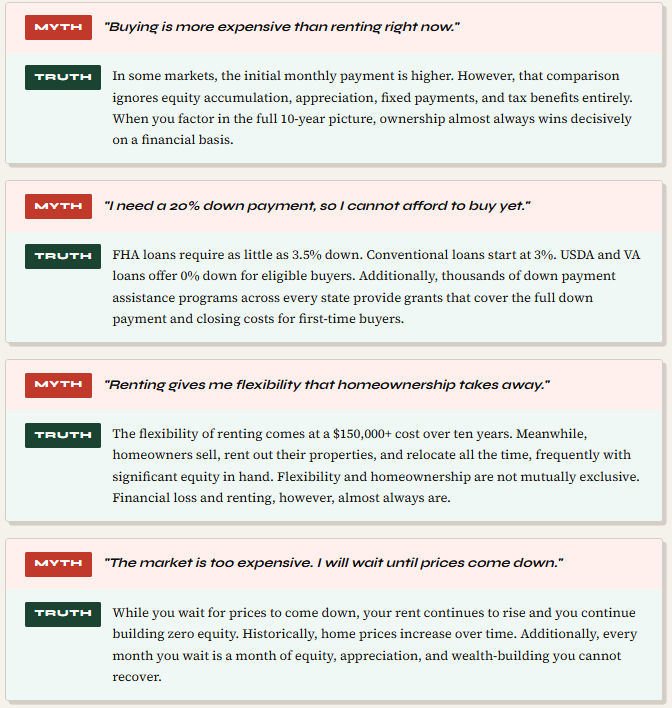

Myths That Keep Renters Trapped in the Cost Cycle

Your 90-Day Path Out of the Rent Trap

The math is clear. The case for homeownership is overwhelming. So the only question that remains is this: where do you start? Here are the five steps that move you from renter to homeowner as efficiently as possible.

- Know Your Credit Score and Report Today. Pull your free credit report at annualcreditreport.com. Know your score across all three bureaus. Dispute any errors immediately. This single step moves more people closer to qualifying than anything else, and it costs nothing.

- Calculate Your Debt-to-Income Ratio: Add up all your monthly debt payments and divide by your gross monthly income. If your result is above 43 percent, focus on paying down existing debts before applying. If it is below 43 percent, you may be closer to qualifying than you think.

- Research Down Payment Assistance Programs in Your State. Visit your state’s housing finance agency website and search for first-time buyer programs. Many offer grants between $10,000 and $25,000 that never need to be repaid. This money exists specifically for people who believe they cannot afford to buy.

- Talk to a Lender This Week. Not to apply, but to understand your options. A 20-minute conversation with a knowledgeable lender will tell you more about your real readiness than months of research online. Most people are significantly closer to pre-approval than they realize.

- Join a Structured Program That Holds You Accountable. The clients who move fastest are not the ones with the best credit or the highest income. They are the ones who have a coach, a community, and a deadline. Marcia’s 90-Day Challenge provides all three. The investment in guidance pays for itself in equity within the first year of ownership.